Details on Malaysia’s EPF (KWSP) Account 1 VS Account 2 withdrawals. The 15 different categories of withdrawals have been divided into Account 1 only, Account 2 only & both accounts withdrawals. Information is for general reference only & is an unofficial summary based on EPF’s official website. Additional forms, documents required & details may not be listed.

Updated: Jan 13, 2021

![]()

EPF Account 1 Withdrawal

Members’ Savings Investment Withdrawal (EPF-MIS)

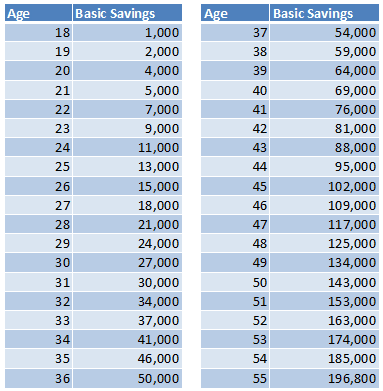

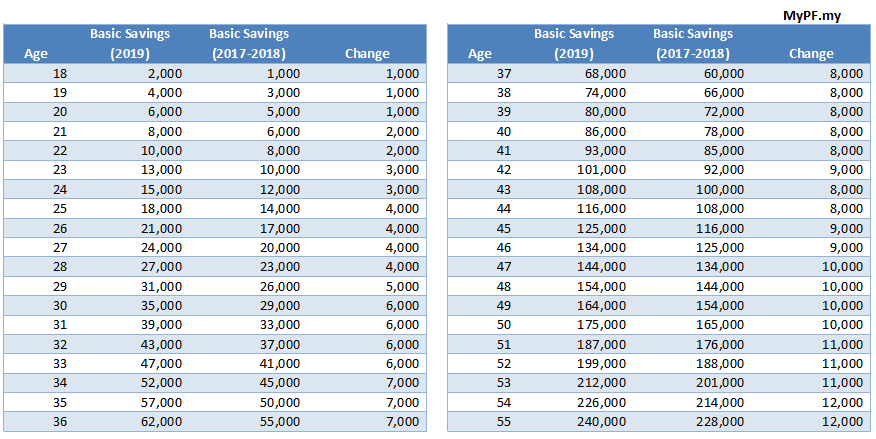

- Effective 2017 Jan 1 with higher minimum Basic Savings amount (Previous minimum Basic Savings)

- EPF approved investment funds only

- Min 3 months from last investment date

- On funds sold, amount returns to your EPF Account 1

- Min 1000 per investment

- Max 30% of amount in excess of Basic Savings (Min balance)

[Formula: Account 1 Ttl – Basic Savings * 20%]

E.g. Age 30 | Account 1 Ttl: 60k

Max invest: 60k – 29k * 30% = 9.3k

{kind=link}

EPF Account 2 Withdrawal

Withdrawal to Purchase / Build a House

- Individual /Joint (immediate family OR no relationship) / Help Spouse

- Age < 55

- Buy / Build Residential (Note: Shop lot with residential unit qualifies)

- Financed through housing loan (EPF approved institution) / Cash purchase

- Not for renovation / 3rd house / overseas property / land

- Min 500

- Withdrawal for 1st or 2nd Housing loan: max 110% of house price less downpayment

- E.g. House price: 500k | Housing loan: 90% (450k)

Max withdrawal: 500k – 450 k * 110% = 55k

- E.g. House price: 500k | Housing loan: 90% (450k)

- Withdrawal for 100% housing loan (Zero downpayment): max 100% of house price

- Withdrawal for cash purchase (self-financing): max 110% of house price

- Max total Account 2 balance

Withdrawal to Reduce / Redeem Housing Loan

- Individual /Joint (immediate family OR no relationship) / Help Spouse

- Age < 55

- Buy / Build Residential (Note: Shop lot with residential unit qualifies)

- Outstanding loan balance from approved Financial Institution

- Not for renovation / 3rd house / overseas property

- Withdrawal for 3rd house allowed only when first or second house is sold or disposed

- Only 1 application per year (from the previous housing loan withdrawal date)

- Total housing loan balance / Total Ac 2 / Min 500

Housing Loan Monthly Installment Withdrawal

- Age < 54 yrs & 6 mths

- Must be Buyer (or Builder) AND Borrower

- Pay actual monthly installment

- Max withdrawal: Total housing loan / Total Ac 2 / Cannot exceed monthly installment payment

- Min: 100 x 6mths

- Allowed to withdraw simultaneously for reduce housing loan balance AND loan monthly installment

- Payment for Refinancing

- Based on original loan balance OR latest loan balance (whichever is lower)

- Not eligible if the original loan balance is fully settled

Flexible Housing Withdrawal

- Process to set aside part of Account 2 savings to Flexible Housing Withdrawal Account to obtain a higher housing loan (aka Ring Fencing)

- Monthly contribution to EPF considered as income

- Savings in Flexible Housing Withdrawal Account CANNOT be used for housing, education, health & age 50 withdrawals

- Released only at age 55 / Full withdrawal (i.e. Leaving Country Withdrawal) / Death Withdrawal

- EPF Annual Dividends will still be given & credited into Ac 2

- Buy / Build Residential (Note: Shop lot with residential unit qualifies)

- Not for renovation / overseas property / land

- Age < 54

- Min savings period of 1 year

- Only for 1 house at a time

- Max application < Housing loan amount

- Transfer: One time (optional) + monthly

Education/PTPTN Withdrawal

- Self / Parent of Child

- PTPTN, Diploma, Advanced Diploma, Bachelors Degree, Masters Degree, Doctor of Philosophy or

equivalent - Local Institutions of Higher Learning:

- Academic (Full time, part time or distance learning)

- Professional Courses

- Vocational Courses

- Foreign Institutions:

- Full time

- Distance learning

- Tuition Fees / Lodging Fees / Study Loan

- Every Semester / Every Year

- Can withdraw multiple times as long as Ac 2 balance remaining

- Can file joint application with spouse for child

- Interview with EPF Officer required

Health Withdrawal

- For medical expenses and/or medical equipment for family members upon critical illness

- Family members: spouse, children, parents (including parents-in-law & step-parents), siblings

- Can make joint withdrawal with family members

- Max withdrawal: Total Ac 2 OR actual medical cost (whichever lower & only on amount not covered by medical insurance)

- Withdrawal can be for EPF approved medical aid equipment (wheelchairs, oxygen therapy, hearing aid, etc)

Age 50 Years Withdrawal

- Age 50-55

- Max total of Account 2

- 1 time only

- Full / Partial (one time withdrawal allowed only)

Hajj Withdrawal

- Age < 55

- Received letter with status Selected from LTH (Lembaga Tabung Haji)

- Insufficient savings in LTH

- Max withdrawal: 3000

Account 1 & 2

Death Withdrawal

- Submitted by nominee

- If no nominee, submitted by administrator / next of kin

- Death certificate & Submitter’s NRIC required

- With Nomination: Full withdrawal

- Without Nomination:

- EPF Account 1 & 2 Total < 2500: Full withdrawal

- 2500 < EPF Total < 25000: 2500 (1st 2mths) & Remainder (after 2mths)

- EPF Total > 25000: 2500 (1st 2mths), 17500 (after 2mths) & Remainder to person who provides Letter of Administration/ Letter of Probate/ Distribution Order (Land Office)/ Faraid Certificate (Syariah Court)

- Compassion additional death benefit of RM2,500 may be given to next-of-kin provided application made within 6 months for Malaysian citizens below 55

Age 55 Years Withdrawal

- Age > 55

- Full / Partial (min 2k; every 30 days) / Monthly (min 250 p.m.)

- From 2018 Jan: Full / Partial (no minimum) / Monthly (min 100 p.m.)

Age 60 Years Withdrawal (Akaun Emas)

- Age > 60

- Starting from Jan 1, 2017 any EPF contributions made from age 55-60 will be into EPF Akaun Emas

- Full / Partial withdrawal from Akaun Emas only allowable upon reaching age 60

Pensionable Employees Withdrawal And Optional Retirement Withdrawal (Public Service)

- Employed in Public Service & emplaced in pensionable establishment

- Optional Retirement from Public Service

- Full withdrawal employee share of contribution including dividends if still have savings in EPF after government share returned to Retirement Fund (Incorporated) (KWAP)

- No longer considered a worker as defined by EPF act

Leaving Country Withdrawal

- Letter of Renounciation of Citizenship (Form K / Form Y) & other documents

Withdrawal Of Savings Of More Than RM1 Million

- Age < 55

- EPF savings (Total Account 1 & 2) min 1.05 million

- Min withdrawal: 50k (from Account 2 & if insufficient from Account 1)

Incapacitation Withdrawal

- Confirmed incapacitated, physically or mentally

- Achieved the level of Maximum Medical Rehabilitation (MMI) to work by a doctor who has examined you AND by a medical doctor in a Medical Board appointed by EPF

- Application supported with medical report dated < 1 year from date application received

- No longer working at time of application

- Requirement to attend interview session

- Additional Incapacitation Benefit from EPF of 5000

- Full

FAQ

Q: How can I check/claim unclaimed monies in EPF?

EPF has launched an online Unclaimed Contribution Information Search.

Q. Is there a limit to the number of EPF withdrawals? For example, if I overlap my withdrawals from Ac 2 to serving housing loan & education loan.

A: You can have multiple withdrawals ongoing. However, it is subject to individual withdrawal limits. For example, you can only withdraw to reduce your housing loan after 12mths from the last withdrawal date.

Note: You can only have 1 home loan withdrawal from Ac 2 at any time

Q: If I bought a property previously financed with Ac 2 withdrawal & later sold it off, would I be able to withdraw from Ac 2 for a new property purchase?

A: Yes. When you sold off your property, you can now apply to withdraw from Ac 2 to purchase your new property.

Q: After I sell my property which had withdrawal of funds from EPF, do I need to return funds to EPF?

A: You only need to return the withdrawal amount if you did not use the withdrawal amount to purchase a house or you have cancelled the purchase of property.

Thus, if you have disposed the property, you do not have to return the withdrawal amount. You may apply for Withdrawal to Purchase a Second House since you have sold or disposed the ownership of the first house. Based from your record, you have made the Withdrawal to Purchase the first house in year 2012. For submission of Withdrawal to Purchase a Second House, you may submit documents for proof of selling first house/disposal of ownership of first house and documentation for second house purchased. For further information, you may click at the link of: Withdrawal to Purchase a House

Q: If a person wanted to, could he/she deposit extra money into either EPF account?

A: Yes you can make extra EPF contributions but only to Ac 1 which can only be withdrawn after age 55. If your EPF annual contribution total is < 4000, you may want to consider making an extra contribution to max out your tax relief. EPF min returns 2.5%. Subject to EPF investment performance. One may want to invest in a vehicle with higher returns/liquidity (FD, endowment, shares, UT, property).

Contributing More Than The Statutory Rate (From EPF website):

You or your employer, or both, may contribute at a rate exceeding the statutory rate through the following options:

If only you opt to contribute at a rate exceeding the statutory rate, you may submit a notice of election to contribute at a rate exceeding the statutory rate using Form KWSP 17A (AHL).

If only your employer opts to contribute at a rate exceeding the statutory rate, your employer may submit a notice of election to contribute at a rate exceeding the statutory rate using Form KWSP 17 (MAJ).

If both you and your employer opt to contribute at a rate exceeding the statutory rate, you and your employer may submit a notice of election to contribute at a rate exceeding the statutory rate using Form KWSP 17A (AHL) and Form KWSP 17 (MAJ) respectively.

This rate will be the new statutory rate and shall remain so until you and/or your employer submit a notice of cancellation using Form KWSP 18A (AHL) and Form KWSP 18 (MAJ) respectively. Upon receipt of the notification, the rate of contribution will be reverted to the current statutory rate.

Q: Can I withdraw from Ac 2 to purchase overseas house, marriage or a personal loan?

Unfortunately the withdrawal is not allowed to buy a house abroad, marriage, personal loan or other purpose not stated explicitly by EPF.

Q: Can I withdraw for my children’s university studies?

Yes for diploma or equivalent & higher studies in academic / professional / skill-based / vocational course in an authorised institution of higher learning. Including tuition fees & airfare. You will need to submit offer letter & other relevant documents.

More info: kwsp.gov.my

Q: Is it true that EPF does not pay dividends if you keep your money in EPF above age 75?

There was a 2008 EPF policy that was never enforced. It has since been amended in 2015 (EPF Enhancement Initiative 3) & dividends kept voluntarily in EPF are given until age 100. Subsequent to age 100, the money will be transferred to Registrar of Unclaimed Monies.

Thanks for posting this. Never really took the effort to find out more about the both accounts. only know about withdrawal for home, and when my agent told me that Account 1 can be used for investment.

by any chance you know or have any info on edu withdrawal?

Is there any mode payment for EPF member which have no bank account..can it like paying in cheque or cash payment voucher?

Hello there

I’ve recently sent all my EPF withdrawal docs. to EPF office from UK. I’m a British national now.

Its been over 4 weeks now and still no news, how will I know the tracking postal number for my Bankers Draft mail when they’ve posted it.

Thank you

I had withdraw from my a/c2 for twice, one has been sold, and one was under abandoned project.

Now I wish to withdraw for my property which was purchased at February 2014.

Can I?

I am 53+ years old. I have housing loan balance rm125k. Can i appeal to use account 1 to clear the housing loan instead still continue monthly installment?

Hi,

Kindly let me know the list of documents need for PF withdrawal for purchasing a house.

More info: kwsp.gov.my

I am considering to withdraw account 2 deposit to fund the house that i recently bought. Just wonder, will i still entitle to any dividend after the withdrawal? i.e. it is already Aug’16 now, will i entitle to dividend on proportion basis? Dividend calculated on daily basis? Or is it better to just wait for the declaration of the dividend before the withdrawal?

Can I withdraw for my emergency debt settlement for my girlfriend… Is that possible..

Hi, I bought an apartment @ RM1.35M and I paid 10% down payment to the developer. I would like to know how much money can I withdraw from my EPF account no.2 if I decided to obtain a housing loan from local bank around 300K.

My EPF account no.2 balance amount is approx. RM650K. Remaining amount will be paid by Cash.

Regards

KL6633

Is KWSP open after 28 April 2020, after

3 consecutive National Shut down period

for withdrawal after age 55?

3rd period of Movement Control Order?

3nd Movement Control Order : 15-28 April?

2nd Movement Cobtrol.Order: 1-14 April 2020?

1st Movement Control Order m: 18-31 March?

Further exrention: 29April-12May ????

LEE, Joy

Can I withdraw the full amount when I reach the age 55? I understand that it’s not possible.

Please clarify.

Can I still withdraw my Epf money after 1st jan 2017. I shall be 59years old.I have the understanding

that with the new acct Emas, there will be no withdrawal of EPF money till 60 years old.Kindly clarify.

Thank you.

Sir/Madam,

Under Pensionable Employees Withdrawal And Optional Retirement Withdrawal (Public Service), Item No. 4 stated “No longer considered a worker as defined by EPF act”.

◘ Can help to elaborate more on this?

◘ Thus one who is self-employed (where no more monthly EPF contributions is made) falls into this category?

Hi, would like to ask about withdrawal money from account 2. I wanted go oversea working, is it possible to withdraw some money

If i withdrew 13 years ago for a house purchase , can i withdraw now for education ?

I will obtain a citizenship from other country soon. Upon submitting all required documents such as IC, passport and EPF withdrawal forms, when will EPF fund will be credited into my bank account.

Pls advise

Thanks

Skin

Hi…

I submit my application twice for i-lestari… My status is ineligible… Reason were wdm0010:the member is not eligible for this withdrawal…

Can i know why is this so… What is code wdm0010?

I have a residence pass (talentcorp) and director/owner of a company in Malaysia for over 10 years. I am 53 years old. I want to know if I can withdraw my full epf at 55 and not have to give up my pass and leave the country? I want to continue the business with my business partner. Information on websites after Nov 1st make me feel that I can withdrawal the full amount at 55. Looking for advice.

I am 56 years old this year and still working. Do you confirm that under akaun emas from 1 Jan 2017, I am only allowed to withdraw RM2000 a month and not lump sum anytime I wish?

More info on Akaun Emas: https://mypf.my/2016/11/03/epf-akaun-emas-changes-from-jan-1-2017/

hi , may i check with you , says i had bought a Commercial and residential unit of condominiums can i withdraw account 2 ?

why keep on change the age to 60? next time change to 80 is more easy.. set for longer..

If I have more than 1.05 mil in EPF, how much can I withdraw at age 50?

I’m 52yrs, I did withdraw acct 2 when 50 yrs, now, I’m no working, possible or any chance to proceed 2 time withdraw ?

I am a foreign national living and working in Malaysia for the last 7 years and I believe that the only way I could withdraw my EPF funds were by leaving the country. However, I read that this has now changed and that I can withdraw payments for housing (in Malaysia), education and health at age 50 and I can also withdraw my full EPF contributions aged 55 from Jan st 2017 – Is this correct?

Hi.. I’m 35 and I was retrenched. I’m applying for job but I’m not getting any offer. I’m unemployed for 8months… Is there any wai I can withdraw my epf to pay my debts…

Hi is the optional retirement applicable for unemployed or self-employed but without any incomes as yet as of age 45 years?

(Translation) Optional Retirement Withdrawal:

1. You have chosen optional retirement from the Public Service and no longer employed OR

2. You have chosen optional retirement from the Public Service and reemployed with a different employer or self-employed OR

3. You have served in a government agency and have opted for retirement under a privatisation or corporatisation exercise but continue to work with the same agency

4. Below age 55

recently going through the procedure to withdrawn money, notice a funny thing. supporting doc for buying a house with cash ” Suratan Hakmilik atas nama ahli; ATAU

Borang Pindahmilik KTN 14A atas nama ahli yang telah disempurnakan oleh Pejabat Tanah ATAU sekurang-kurangnya Borang Pindahmilik KTN14A telah lengkap ditandatangani berserta resit penyata perserahan oleh Pejabat Tanah”

so they expect u buy a house that under your own name?

and in order to submit the change of name u need to paid the seller 100%. then why u need EPF then?

Can I withdraw the entire Account 2 for postgraduate studies at one time & get it all paid to the University without monthly instalment?

Or is there a limit?

Hi can I withdraw my epf for house renovation. What documents should I provide.

Hi..i will be 55 years old on August 2020. can i withdraw my EPF saving earlier on July?

I noted that dividend credited in March every year has no compounded dividend for the year of crediting. For example, dividend for year 2018 credited in March 2019 did not earn any dividend in 2019. Will you be able to verify whether this is true?

I recently bought the house and its was my first house. Am I entitled to withdrawal 100% from my account 2 because I loan 100% from bank? For first timer withdrawal for buying house, is it the money goes in my account?

Hi,I would like to know when I reached the age of 50, can I withdraw all my account 2, while I am still employed? Will EPF issue me a cash cheque/bank draft as I have no account with any bank? And when can I approach EPF to submit or request in advance for my withdrawal, eg.i will be 50 years in June 2017. Your information will be much appreciated TQ

Hi ,Good afternoon and thanks for you fast respond on my earlier post,can EPF issue cash cheque under my name ,so as once I cash out I can then banked into my son account, as I was rejected by banks to open up a saving account,as I understand EPF will not issue Bankers cheque under my son name right?,your advice is very much appreciated TQ

Hi there

If one withdraws under the “Leaving Country” category, will dividends be paid up to date of withdrawal eg. 30th Sept 2017, or up to 31st December 2016 only?

If it is up to date of withdrawal, would the rate of dividend be the 5.7% that was declared for 2016?

Cheers

Tom

I am in amidst of applying Leaving Country Form. Requirement is to surrender my NRIC. My question is, do I have to surrender my Malaysian passport as well?

Hi, was considering retiring by 50 hence I wonder is there a possibility to request EPF to disburse previous year declared dividend on monthly basis upon reaching age 50 to sustain my living cost?

Thanks

Hi, was wondering if i can withdraw for my dad’s knee cap replacement operation?

Hi,

I purchased a property in 2013 and took a 90% loan but the loan has not yet been fully disbursed therefore, i’m currently still paying interest. Will I be able to withdraw from EPF Acc 2 to serve the interest and thereafter the full installment once it’s fully disbursed?

Thank you

Hi,

Can we opt for early retirement before age 45 instead? What is the proper forms and procedure guidelines?

Thanks.

Link to forms/guidelines: http://www.kwsp.gov.my/portal/en/web/kwsp/member/age-50-years

Hi

If I do a full withdrawal upon attaining the age of 55 in Sep 2017, will EPF still credit the dividends into my account after the dividends is declared in early 2018 after the financial/calendar year ends ?

Thanks.

More info: http://www.kwsp.gov.my/portal/en/web/kwsp/member/age-55-years-withdrawal

Can withdraw from 2nd acc. fully for car purchase?

I had withdrawn once from Acc 2 for the 1st house in 2013 (the S&P under my name and wife but loan is under my wife – Govt. loan). I bought another house in 2015 (loan facility 90% & under my name), but now still paying interest every month (progressive pays since the loan not fully disbursed until house fully built). Can I withdraw the money from Acc 2 to pay this monthly progressive payment?

Hi, Can i withdraw my epf acc 2. Fyi, i already utilised my acc 2 for a monthly payment of my home loan and just finished last february. Can i apply again for a 10% deposit of the same house for a house i bought in 2012 . I never claim a 10% deposit for this house when i bought it in 2012. Kindly advise.

Good day,

I have made a withdrawal from EPF Account 2 in 2016 to pay off some amount of PTPTN loan. Just few days back, I applied for a second withdrawal, but some work came up and I had to leave to overseas immediately. I’ll be away for 3 months, and it looks like my second withdrawal will not be successful.

My question is, when I come back, will I be able to make a third application of withdrawal to pay off some amount of my PTPTN loan again?

What are the max amount of times I can withdraw from Account 2?

Please advise, thank you.

I’m an ex citizen, Ive submitted my withdrawal documents. I’ve emailed them and no one bothers to reply.

My question, I cannot log on to check my balance, does that mean once the Bankers Draft is done, they also close Iakaun .

That’s why I can’t log on anymore.

I’m a first time buyer, Intend to buy a house for 340k, how much maximum allow to EPF withdrawal for purchase?

My ac2, now with approximate 70k, can withdraw full?

Hi my mum this year will be 53 years and not working any possible withdrawa.from 1 acc to personal use

Hi, i’m a malaysian and my husband a PR. we r planning to buy a house but only my name will be on d spa. how can we use my husband’s epf (1st time withdrawal) for the purchasing of this hse? in cases like ours, can the money be disbursed into his savings acct?

Hi:) my question is ,if im 54 yrs old ,and i have already took some amount from my acc 2, at age 50 once, can i withdraw some money for my child education purpose .If the answer is yes, then why is it not possible for me since, one of the officer called and said that they can only provide partial money like 4K .and said can only withdraw next year ?

EPF Education Withdrawal Eligibility:

(i) A Malaysian Citizen; OR

(ii) A Malaysian Citizen who has made Leaving The Country Withdrawal before 1 August 1995 and later opted to re-contribute to the EPF; OR

(iii) A Non-Malaysian Citizen who:

Has become an EPF member before 1 August 1998; OR

Has obtained a Permanent Resident status (PR).

Have not reached the age of 55 on the date the application is received by EPF; AND

Still have savings in Account 2.

yes i do have enough savings in account 2 to fund my child education . so its really weird when i hv encountered this kind of situation . so can i make a reconfirmation ? so if i took some of the amount from acc 2 at age 50,and i still can withdraw money from age 54 but under education fund right ?

Hi, I would like to know if i am buying a property with joint name. So when I get the SNP, can I and my partner fully withdraw amount from our account 2?

Hi.I‘m intend to purchase my first property for Rm388K under government affordable house scheme.For this case,can i withdraw from epf for the downpayment (rm38k) under my husband and my name account in epf ? Can i withdraw more than Rm38k? will they transfer the withdrawal amount to bank saving/current or loan account for first time withdrawal?

I would like to withdraw EPF money to build a house but the house will be built on land that is still in my father’s name… Is it still possible to withdraw the EPF money or does the land have to be transferred to my name first? Thanks

Hi, I have a epf account and I’m retired. I’m 68 this year. Could I deposit money into epf account!

Where can I get a full list of the mental medical conditions that are accepted for the Incapacitation Withdrawal. All the information I can find is very general and vague.

Thanks.

http://www.kwsp.gov.my

With 1MM saving in EPF fund, is it best to do a enhancement partial withdrawal when you reach 55 to sustain a 8k monthly spending until the age of 85?

Upon death of a member, can the nominee opt not to withdraw the money immediately but only after 15 years later (member age will still be below 100 years old at that time)? Will the account be still active and generate dividends?

Hi,

I want to know can I withdraw money from Account and invest in FD??

Sir if blacklisted can withdraw from acc 2

Hi,

If a person who is ,unemployed at age of 50, and struggle to pay for housing loan. can withdrawal money from his 2nd account to pay the money?

how about 1st account can withdraw for pay housing loan?

I am a foreigner working in Malaysia and holding resident pass. I am contributing to EPF together with contribution from my employer . Now my age is 56. Can I with draw my EPF money?

I am not leaving the country; but wish to take my EPF amount. Is this possible?

Hello,

I am a foreigner and would leave the country some time in Jan 2018. In that case, since the Dividend rate for 2017 would still not be declared, would I only get the total amount accumulated till date ( Jan 2018) and my dividend income for 2018 would be lost :-(

Also, if I apply for withdrawl in Jan, and if the whole process takes 1 month and within that month, if the dividend is declared, would I get it ? I just dont want to lose the 5 .5 % ( Approx) income on my corpus.

I hope I explained my situation. Any help would be appreciated.

Hi,

I want to know can I withdraw money from Account 2 and started business?

Hello,

Thanks for the insight!

As I read that “Not for 3rd house” in this article, below my case:

I had made a withdrawal from Acct 2 in Aug 2015 to July 2016 for “Housing Loan Monthly Installment Withdrawal”, where EPF deposited the payment to my personal account.

Now that I made a purchase on 2nd house, can I withdraw to pay my down payment? FYI, first house still yet to be disposed (not intend to).

Hi,

If i pump in money in January 2018 into KWSP, would i enjoy the dividend declare on February 2018?

Hi could i redraw my epf to settle my akpk

hi,

Looking to buy my 1st property , would I be able to withdraw my acct 2 to fund the 10% down-payment ? or pay first and get back from EPF acct 2 ?

Hi..I have a 8 year old son and 3 month old daughter. .will I be able to do epf accts withdrawal no 2 for their future education purpose now.. TQ S.R.

Hi there.. I have already withdrawn certain amount from my account 2 for my first house which I bought in 2015.. Can I withdraw again since I haven’t reach my 100% amount? Thanks in advance for your reply :)

Upon attaining age 50, I know you can withdraw from Account 2. May I know if a bankrupt can withdraw it as well?

Hi, my house loan in under my sister’s & my name. Can both of us withdraw from our AC 2 to settle the loan?

Hi there, just wanted to check am I able to withdraw my 2nd account for housing loan repayment which is under my parent name ? The house is under my mom’s name and she’s currently unemployed. Thanks in advance :)

Good Afternoon, I just wonder can I withdraw money from Account 2 to purchase PC? Thank you.

Hi, I have been unemployed since 2016 and I am 53 years old now. Can I withdraw from Account 1 either all or partial amount? I cant get a job and it has been a struggle to survive. Readings all the answers, you have mentioned that a one time withdrawal either partial or full can be made at 50 – 55 years old. Please confirm if this is one time withdrawal is from Account 1.

I have withdrawn previously from Account 2 to pay for my housing loan. I dont have much now to withdraw from Account 2. So I can withdraw partial/full from Account 1? I just need a confirmation if I can withdraw from Account 1 since I have withdrawn from Account 2 previously. If I can, this will save me from adding on to additional debt. I cant get a loan, banks are not in favour to review or loan amount.

I wish to let you know that KWSP will only allow withdrawal from Acc 1 at the age of 55 to finance the cost of livibg during retirement. I had a confirmation from KWSP today.

Source: http://www.kwsp.gov.my/member/withdrawals/partial/age-50

Can ask specifically why it’s not allowed under age 50 withdrawal. All the best!

I wish to let you know that KWSP will only allow withdrawal from Acc 1 at the age of 55 to finance the cost of livibg during retirement. I had a confirmation from KWSP today.

Hi, I was told that if you withdraw from EPF Account 2, you will need to pay the amount withdrawn back? Is this true?

An aunt was telling me this, saying that if I withdraw from Account 2 then I will need to pay the amount withdrawn back or else they will deduct the amount withdrawn + interest from my Account 1 to recover it and that it will only happen once I reach age 55. Would just like some clarification on this.

Thanks.

There are several documents need to be submitted for the withdrawal to purchase a house. Does the EPF Act or its regulations have provisions requiring the relevant documents that are to be submitted? If yes, can you please state the relevant provisions. Thank you.

http://www.kwsp.gov.my/ms/member/withdrawals/partial/purchase-a-house

Hi, my first house is still under construction, i have made a withdrawal last year to reduce the deposit payment. Can i make another withdrawal from the same Acc 2 this year?

hi, if i already withdraw 2nd acc to pay downpayment 7years ago for my home,

so now can i withdraw again 2nd acc money to help my wife for buy new house under her name?

Hi,

Previously i was paying my monthly housing installment using KWSP money, and recently I have changed from ambank to alliance bank. What are the documents needed for KWSP so they can transaction to my alliance account.

More info: https://www.kwsp.gov.my/member/withdrawals/partial/housing-loan-monthly-installment

Hi,

I wonder how the installment redrawal work in term of overlapping? For eg, currently I have monthly Installment redrawal which end December, then I apply another application of monthly Installment and got approved now, and the new application redrawal will credit to my bank account after the current one ended(Jan), or I would get 2 redrawal during December?

Hi,

Would like to clarify if I already withdraw my Account 2 by age 50 on June 2020, Am I still entitled for dividend on 2021?

Can I withdraw from my acc 2 to pay for my daughter’s elementary school? I am a foreigner

Hi there,

I am a foreiner, Could i withdraw fund from acc 2 to buy a house in my country under my name or my wife’s name. Thanks

May I know how long I can have my money in EPF while still receiving the yearly dividends. Is it till 100 years as well? TQ

Hi

I am bankruptcy recently and no job, I need some cash for my living expenses. currently i left less than 5 months to age 55. I have done 1 withdrawal at account 2. Can I get cash from EPF. Or any finance can help me to get some cash out. I have over RM500k in acct 1.

Hi, I am renouncing my Malaysian citizenship and no longer live in the country. Can I leave my epf savings in the account and still receive dividends?

HI Can I have my tax relief if withdraw epf funds for my education?

how often can I withdraw from EPF once I hit a million RM.

Say I have RM 1.05mil in my epf account. Can I pump in an additional 200k in my EPF towards year end and withdraw the 200k after getting the dividends? This way I can get min 2.5-5% epf dividends, which is better than the FD rates now. Thanks!

Hi..

Can i use my epf account 1 to build a house at my hometwon.coz my account to oredy use for my education.now i am jobless..

Can I withdraw partial of my epf I am age 59 due to termination of work coz business is bad

Can I give power of attorney to my sister to withdraw money from my EPF account since I no longer live in Malaysia as I currently reside outside of Malaysia.

my application is rejected and the reason is wdm0010/ What is this ?

Hi, im trying to withdraw for i lestari, the first time it was approved and already paid to me, but for the second month I tried to withdraw again, it states im ineligible. May I know whats wrong?

Hi, I applied for I Lestari but status ineligible WDM0010 what does it mean ?

I bought a house with my friend and loan was approved under both names. Can my friend and I withdraw from our own epf account since there’s no proof of relationship?

Hi I nominated my husband 70% and my son 30% as my nominations. What happens upon my death will kwsp release the money according to my arrangements ? If I nominate for my son to get 100% of my money will kwsp give my son the 100% or my husband too get if he’s not nominated tq

Hi,

I’m a bankrupt since 2010. Total due is 75k.

My question is, can a bankrupt pursue studies abroad? Second, can I withdraw from my EPF account 2 to fund the studies? I have 80k in my 2nd account with EPF. Since I lost my job due to Covid, this is a good time to gain higher qualification and to come back and earn more to eventually settle my debts.

After signing S&P, the buyer pays me nothing and wants to apply EPF account 2. Only on getting EPF account 2 money, the buyer will pay me the 10% of S&P agreement. Question: EPF will pay to who, buyer or seller?. Can the buyer gets his EPF money and refused to pay the seller ( a trick to withdraw EPF account 2)

Hi,

Is it possible for an expat to withdraw from the EPF from outside of Malaysia? For instance, if I left the country at short notice and couldn’t come back, would it be possible to do the withdrawal process from a different country?

I am a bankrupt age above 55years old. and without a bank account.

How does it work with epf withdrawal?

If my i want to close my akaun..can u suggest method..because i have only rm3000 only in that account.

Hi we recently bought a property. The Property/S&P is under my wife’s name. However the loan is under my name as primary loan applicant and my wife as supporting (as she is a housewife). Can I withdraw my epf acc 2 if my name is not in the S&P and only in the loan document?

When you said you can withdraw all money in account 1 at age of 55, you mean on the year you are 55 or after your birthday at 55 ? For example if I born in 1965 Dec 10th, I can go to withdraw any day from 1st Jan 2020 or after 10th Dec 2020) ?

Hi my dad is due for a hip surgery. Can I withdraw from account 2 for his surgery cost

My S&P date is 16 July 2016 and the house is still under construction now. Am I eligible to the “Withdrawal to Purchase / Build a House”? My monthly instalment has not started yet.

I previously withdrawn from my acc2 for my house 1st loan. Subsequently, I refinanced a 2nd loan under the same property. I have since pay off the 1st loan but 2nd loan still outstanding. Would I still be eligible to withdraw from my acc 2 to reduce the 2nd loan? Is there any possibility you would think that I may not be able to do that although I have sufficient balance in my acc 2 & have not withdrawn any since more than 12 months ago. Thank you.

I previously withdrawn from my acc2 for my house 1st loan. Subsequently, I refinanced a 2nd loan under the same property. I have since pay off the 1st loan but 2nd loan still outstanding. Would I still be eligible to withdraw from my acc 2 to reduce the 2nd loan? Is there any possibility you would think that I may not be able to do that although I have sufficient balance in my acc 2 & have not withdrawn any since more than 12 months ago. Thank you.

hi can i withdraw EPF from Account 2 for my third house, refer to followings scenario:

1st house, joint loan under 3 person (father, mother,and myself), loan amount fully settled, but haven’t sold this house yet. – i never withdraw EPF for this house

2nd house, also joint loan (me & my spouse) – i have withdraw EPF for this loan year 2013 for downpayment.

3rd house, loan & S&P under my name, my spouse as guarantor. – can i & my spouse withdraw EPF for this house?

HI, can i withdraw epf from form account 2, for my third house with following scenarios:

1st house – joint loan with family (father,mother and myself) – never withdraw epf for this house, loan fully paid – have not sale this house yet,.

2nd house – joint with spouse – i have withdraw from account 2 to pay down payment in year 2013.

3rd house which is not ready yet – loan under my name, and my wife as guarantor for loan – can i withdraw epf for this house?

Hi, I’m planing to buy my second house and would like to know if I can withdraw from my account 2 to either reduce the loan amount or for making monthly installments. I was told that I can withdraw to make monthly installments only for my second house.

I have previously withdrawn from my account 2 for my first house to reduce the loan amount and the house is still in my name under mortgage.

Appreciate your time in answering my questions.

Thank you and regards.

hi,

last two year i withdrew acc 2 for purchasing a house… however at the end i used the money to pay off my ptptn loan instead. can i still withdraw to finance my 1st house?

Hi can I withdraw my epf acc 2 for business?

Hi, I wish to withdraw by 55 year next year 2021. I have invested in Unit Trust using EPF withdrawal money over the years. So, if I sell all my Unit Trust investment this year 2020, the proceeds money will go back into my EPF account rite?? Will I still entitle to get dividend for 2020, when they/EPF declare in next year 2021 for this Unit Trust proceeds money portion too?

My next question is, if EPF declare dividends only in February 2021, if I withdraw all my EPF money in Jan 2021, so do I still get my dividend for the year 2020?? Thank you.

I have been living in New Zealand for the past 13 years under Residence Visa. I am 55 this year and wanted to comeback to Malaysia to withdraw my EPF in full. Unfortunately with Covid 19 the borders are closed and I am wondering what would be the best way to withdraw my EPF?

Hi, i have planned to purchase an apartment. If the S&P is under my name and my husband name BUT the loan is under my name only. Can my husband withdraw his epf acc 2 to purchase the apartment?

Hi, may i know if i don’t withdraw all my money when i reached 56years old, can i continue to withdraw it at age 56? Before age of 60

Hi, are there any EPFO of 75% withdrawal of 1-month unemployment in Malaysia? Please clarify, thanks

Hi, i would like to find out if it is possible to withdraw my EPF as i no longer work in the country. I am still a citizen but reside overseas now.

Thank you for your help.

Hi recently bought condo 730k and loan under my wife 85%.. Can i withdraw my epf acc 2 under buy new home withdrawal? She will also withdraw from acc 2..whats the limit we can withdraw?

I am considering to withdraw account 2 to fund the house that i recently bought. am i still entitle to any dividend after the withdrawal? Am i entitle to dividend on proportion basis? Dividend calculated on daily basis? Or is it better to just wait for the declaration of the dividend before the withdrawal? When is the dividend payout?

Which type of withdrawal is better? The monthly withdrawal for my housing loan installment or a sum from account 2 which we can withdraw once a year. Which one will effect the least of the dividend that I’m supposed to get?

I don’t want to loose too much dividend while withdrawing my money to service my loan. Pls advise. Tqvm

Upon reaching 55 and retired, if you do not withdraw your epf, will you be getting the annual dividend declared or will you be getting a lesser dividend for account 55 or accommodation emas?

Hi

House loan fully under wife name but husband withdraw EPF. The withdrawal will knock off for principal or will cover monthly installment.Kindly advise.

Hi. I am asking on the withdrawal for house purchase. Can my spouse withdraw his epf, if the S&p is only under my name?

Hi can I apply for withdrawal twice from my 2nd account under i-lestari if my 2nd account balance is still more/eligible more than RM500.

An EPF pension was contributed when I was a Government servant in Malaysia. If this is withdrawn now as a British Citizen, would it still be tax free in Malaysia?

My mum is giving me her 40year old single story terrace house (Property remains under my mother’s name).

Current plan is to teardown and construct a new 2story terrace house on the plot of land.

Can i withdraw from my account 2 to settle some of the construction cost? If yes, what’s the procedures and documents required?

Thank you

https://www.kwsp.gov.my/member/withdrawals/partial/build-a-house

IWe still continue earning yearly interest as long as we have balances in EPF? Up to what age? The yearly earned interest post-retirement is taxable?

Hi, I am a foreigner who left country recently. I have withdrawn my EPF balance. But my company is still yet to deposit to EPF the last employee and employee of my last payroll. There is also annual bonus coming in March 2021 which I normally would have employer EPF share too. Can my company continue depositing in my EPF account?

Hi,

Can I withdraw from Acc 2 in smaller sums multiple times for the down payment for the same property as long as it doesn’t exceed the threshold?

Hi,

Would I be able to withdraw COMPLETELY from my ACC 2 for the down payment of my 1st properly?

Hi there, my S&P’s stamped date was in Feb 2018 but I signed the S&P in August 2017. Can I still withdraw the money in Acc 2 in Jan 2021? Due to COVID-19, I’m stuck in hometown since MCO and only had the chance to get my documents ready now as they were in another state. Unfortunately, EPF only allows appointment and the earliest slot is in the third week of January 2021. If it follows the stamped date, I am still within the 3 years limit but if it follows the signing date then I will be in trouble. :( I didn’t expect that I will be stuck in my hometown for more than 9 months in this year. Appreciate your advice. Thanks.

Hi, i’m planning to withdraw the money from Acc 2 for my down payment for my 2nd home. FYI, I did not withdraw any amount from EPF Acc 2 for my 1st home.

Can I still able to withdraw completely from my Acc 2 for my 2nd home?

I’m midway of bankruptcy proceeding, currently don’t have bank account and jobless. Do I entitled to apply for Isinar and do they issue cash cheque when my withdrawal is approved.

Hi, im a foreign student studying in malaysia and im doing a case study on retirement and EPF. I would like to know if the EPF continues to pay dividend into the account after the age of 55 and what are the dividend rates and if they are afftected by inflation rate.

Hi.. I have utilized my EPF Acc2 twice for my first and 2nd house, and recently i have just sold my 2nd house. Can i withdraw my EPF Acc2 as in to Purchase my 3rd house?

Hi, I want to ask about why the i-lestari i’m successful got RM200.00 up to 8 months (May’20 – Dec’20), but suddenly January and February status is ineligible (WDM0010)?

Can withdrawal of the money deposited under Self Contribution be done at any time?

If I buy a house from developer, the snp and loan agreement both under my name, i am single, can my sister withdrawal from account 2 to finance for that house even thought she legally is not owner?

i’m a foreigner, who is leaving malaysia on June 2021 – and had been contributing to EPF for a number of years. I dont want to withdraw my epf if i leave malaysia. can i keep my epf here and allow to earn dividends? i am planning to just keep my epf account untouched for more than 5 yrs

Hi, i am planning to buy a house jointly with my husband.

Can both of us withdraw from our EPF acc 2? Is there any withdrawal limit for joint house?

I am a Malaysian who lives overseas & have no income in the country except for rental income. Can I still contribute to EPF? I have an account since I worked in the country before moving overseas for work.

Good day,

I’m looking to buy my 1st property, upon signing the S&P, would I be able to withdraw my EPF acct (2) to fund the (10%) down-payment ? or it is a must to pay first and apply back from my EPF acct (2) ?

Hi. Thank you for your help. I am 46 n have lost my employment about 2 years now. I then became a full time mom. But I want to apply for the optional retirement withdraw now. Needless to say, our household income is very much affected thanks to Mr. Corona, n our mortgages are, well – unpaid. Can I opt for this to make a full withdrawal? How do I do it? Thank you.

Hi,

I’ve bought my first property RM1.1M.

Total bank loan amounts RM968,435.

Can I fully use my EPF Acct 2 to pay the 10% Deposit @ RM165K

I’ve balance RM250K in EPF Acct 2.

Can I request to drawdown RM200K from my EPF acct.2

Hello, I received my last i-Sinar withdrawal last month and I have several thousands left in my second account. I lost my source of income and no longer have any saving left. My question is, is there any way for me to make more withdrawal for cover my expenses- rental, bills, etc while I am still looking for jobs? Without this withdrawal, I may not be able to live long enough to withdraw it at the age of 60. Im tired of people telling me that I should really think about my old retirement days, about my future. But hey, if Im not be able to survive now, how can I have that future they are talking about?

Hi, i have renounced my Malaysia citizenship last year. Now i am Australia citizen. i am decided to withdraw all my EPF money. i have form-k with me now. As i understand EPF Malaysia office are shut down due to pandemic. What should i do? on your website i need to certify all my forms by Malaysia Consulate in Melburne, i will do that soon but i do not want to just courier back by post i’ll afraid documents may misplaced. Is there any other way i can subtmit the forms? thank you.

Hi. I am 55 year old expat in Malaysia. It seems I am unable to make an EPF nomination (not member before 1998). Is this true and what complications will arise if I die?

Hi, I’ve applied I-SINAR via EPF ACC 1, can I still withdraw completely from EPF ACC 2 for the down payment of my 1st property?

Hi. Can I reduce my housing loan with my EPF? Or is it better and less hassling if I just make a partial withdrawal at age 50 for this purpose to avoid the hassle of documentation, etc? Just wondering.. Also I have named my spouse and child for the nomination. My spouse’s passport number has yet to be updated even though I had edited it on my I Akaun.. I really don’t want to increase my risk of going to the branch just to get my spouse’s passport number updated. Can you clarify how else I can get this done? I have contacted EPF but they did not reply. Thanks.

Hi I am 63 years old , although working, I am not contributing to the EPF, but my employer is,

I wish to withdraw a very small amount maybe around Rm5000,Will EPF will allow it

Hi we can withdraw the excess after reaching RM1m right…? Is this RM1m calculated from account 1 plus account 2 or just account 1…? So if i have account 1 plus account 2 = Rm1.5m, can i withdraw the Rm0.5m excess yearly?

Hi,

im currently doing own business, and would like to contribute I-saaraan/ self contribution to my EPF acc.

my question is, can i contribute more than Rm60’000/ annual into EPF? assume i contributed RM70’000 into epf, what will happen to additional Rm10’000?

Hi, if my snp and loan dont have my husband name, is it possible my husband withdraw money from epf under assisting spouse for reduce housing loan?

Hi. I have two questions.

Previously the house we are staying is purchased under my wife’s name. Can I withdraw from account 2 to help with the monthly installments?

Secondly I am planning to leave the country but not ready to renounce my citizenship as Malaysian since I have yet to obtain citizenship from the other country. Can I make full withdrawal even before reaching age of 50?

Thank you.